Your credit card company loves you.

They know that the psychological tricks built into credit card spending will make you spend more, save less, and build wealth slower. They’re counting on you thinking you’re being clever while they profit from your behaviour.

You know the drill:

- Tap your credit card for everything and get those sweet, sweet points.

- Park your money in an offset or high-interest savings account.

- Sweep it across at the end of the month.

- Feel smug about gaming the system.

But here’s what the banks know that you don’t: this strategy is making them rich and keeping you from making meaningful financial progress.

Can You Beat the Points Game?

Now, yes there are absolutely people who genuinely come out ahead with credit card points.

These are the folks who live and breathe points hacking, track every bonus offer, maximise category spending, and treat it like a part-time job. They’re essentially trying to beat the casino at its own game.

And some of them do win. But they’re few and far between.

The majority of families we work with aren’t in the business of points hacking. They’re in the business of juggling life responsibilities, keeping up with expenses, and trying to put something away for the future. They don’t have time to track rotating bonus categories or calculate the optimal credit card for each purchase.

For these families – which is probably you – the points game is a distraction from what actually matters: building wealth.

The over-spending trap

Research consistently shows that people spend approximately 12-18% more when using credit cards compared to cash or debit cards. This happens even if you religiously pay off your balance every month and swear you never pay interest.

The psychological reason is simple: credit cards create distance between you and your money. When you tap a debit card, you’re spending real money from your actual account. When you tap a credit card, you’re spending tomorrow’s money, which feels less real and less painful.

The real cost of chasing points

Let me paint you a picture of what this overspending actually costs you long-term.

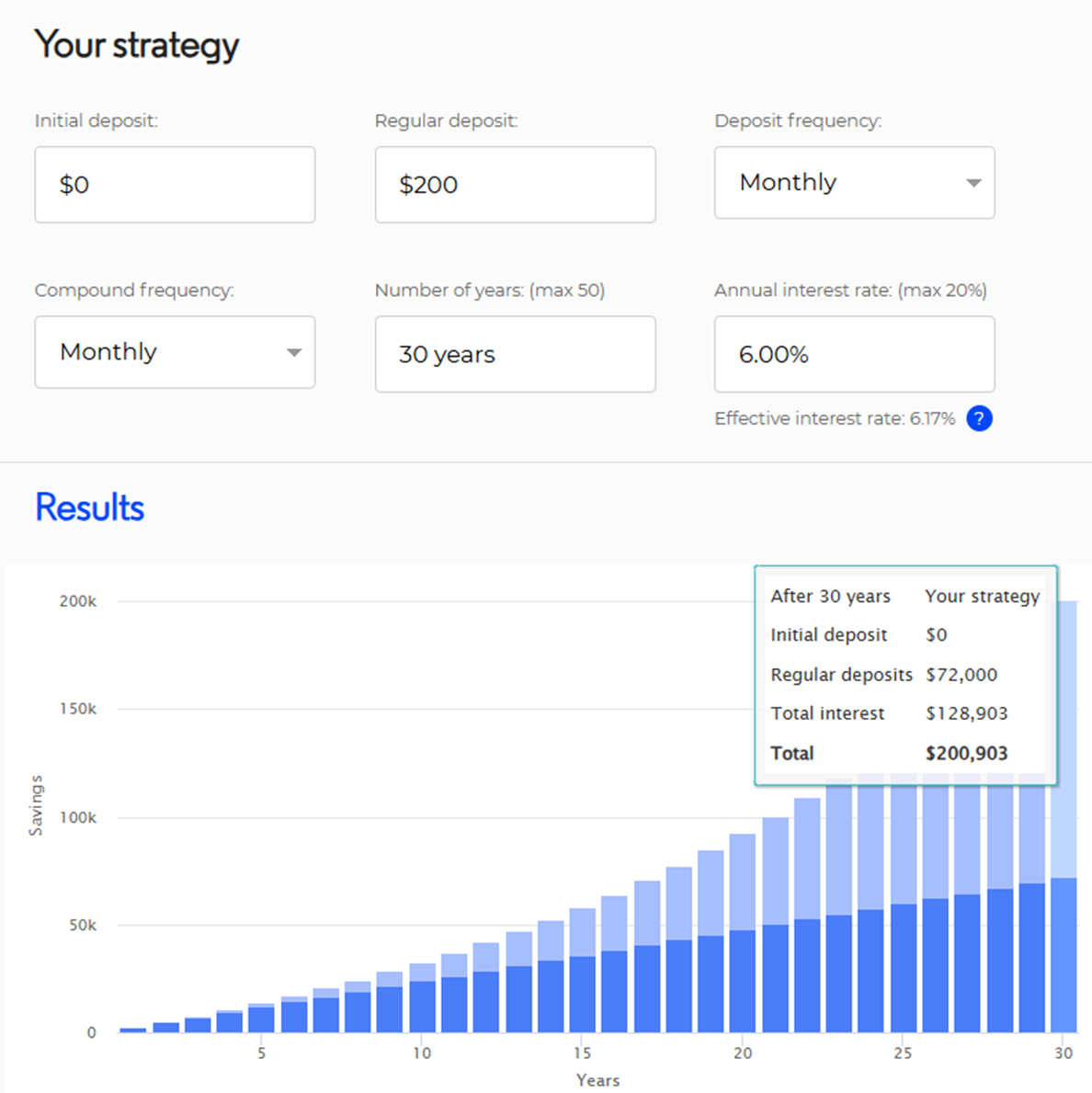

Say you’re overspending by $200 a month because of credit card behaviour. That might not sound like much, but if you invested that $200 monthly at 6% returns instead, you’d have an extra $200,000 after 30 years.

Meanwhile, what did those credit card points get you? Maybe a toaster. Or if you’re really crushing it, return flights overseas.

Half a million dollars versus a few overseas flights. Your call.

The willpower depletion problem

But the credit card trap is just one piece of a bigger problem: most people are manually managing their money, and it’s exhausting.

The average Aussie makes 3,500 decisions every day. What to wear, what route to take to work, what to feed the kids, which emails to answer first. By the end of the day, your willpower is shot.

This is called decision fatigue, and it’s why you find yourself standing at the Coles checkout, trying to quickly transfer money between accounts while a queue of people stare at you. It’s why you swipe the credit card instead of checking your account balance. It’s why good financial intentions fall apart when life gets busy.

You can’t rely on willpower to manage your money effectively. You need a system that works even when you’re too tired to think straight.

The money flow solution

Here’s where everything changes: automation.

Instead of manually juggling money between accounts, you set up a system where every dollar has a job.

✔️ Bills get paid automatically.

✔️Savings happen automatically.

✔️Spending money gets allocated automatically.

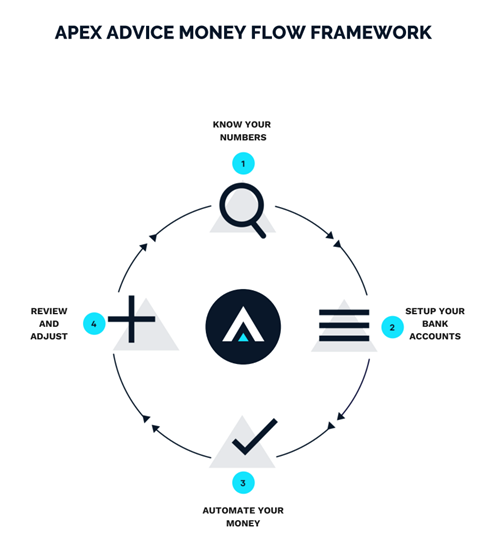

Here’s how it works:

Step 1: KNOW YOUR NUMBERS

Get crystal clear on your cash flow Most people have no idea where their money actually goes. You need to map out every dollar coming in and going out using a proper financial dashboard. You can use our Money Flow Planner to do this – click here to download our Money Flow Playbook and Planner.

Step 2: SET-UP BANK ACCOUNTS

Set up isolated accounts for isolated purposes Instead of one big account where everything gets mixed together, you have separate accounts for bills, spending, holidays, and savings. Each account has one job.

Step 3: AUTOMATE YOUR MONEY

Automate the flow Money moves between accounts automatically based on your predetermined plan. No willpower required. No manual transfers. No thinking about it at all.

Step 4: REVIEW AND ADJUST

Ditch the credit card. Use a debit card linked to your spending account. If you find that you’re transferring between accounts each month, adjust your amounts.

Why the bank’s advice doesn’t work

Banks love recommending credit card sweep strategies because they know the behavioural data. They know you’ll spend more. They know you’ll occasionally slip up and pay interest. They know that even if you don’t, you’re not optimising your cash flow for wealth building.

The popular budgeting percentages you see everywhere (like the 50-30-20 rule) sound great in theory, but they fall apart in practice. I’ve worked with thousands of clients over the years, and I’ve never met two people with the same cash flow situation.

Everyone’s at a different life stage. Everyone has different income, expenses, kids, circumstances. So how can we apply the same formula to everyone without considering their unique situation first?

The three questions that matter

Instead of following generic percentage rules, ask yourself these three questions about your current money management system:

- Is it simple? Can you understand and maintain it without a finance degree?

- Is it sustainable? Will it work when you’re busy, stressed, or distracted?

- Is it scalable? Can it grow and adapt as your income and circumstances change?

If you answered no to any of these, you need a better system.

Future you will thank you

Here’s the beautiful thing about getting your money flow right: small improvements compound into massive results.

An extra $200 per month in surplus might not feel life-changing today. But invested over 20-30 years, that small monthly surplus becomes serious money that opens up real choices.

Future you will be doing a happy dance because you cut up that credit card and redirected money you didn’t even know you were overspending towards building real wealth.

If you’re ready to ditch the credit card trap and set up a money flow system that actually builds wealth, it all starts with having a conversation – book a 15 minute chat here.

Stay Beautiful!

John Manserra

Certified Financial Planner®, Director

Apex Advice – Geelong Financial Advisers for professionals and tradies who want to organise, grow and spend their money with confidence.

👉For more of the good stuff you need to know to organise, grow and spend your money with confidence, subscribe to The Stash newsletter.

👉Download our Money Flow Playbook for a practical framework to make money progress.

Important:

This is not tax advice. Your personal objectives, needs or financial situation have not been considered when preparing this information.

The information contained in this update has been provided as general advice only. The contents have been prepared without taking account of your personal objectives, financial situation or needs.

You should seek advice before making any decision regarding any information, strategies or products mentioned to consider whether that is appropriate to your own objectives, financial situation and needs.

Current at 25 August 2025